US Research Trip: 2018

As part of our ongoing research effort, we recently travelled to the US to better understand the economic conditions on the ground and the implications that would have on our investee companies and the portfolio in general. We have broadly tried to see the same group of corporates that we have seen in the past to ensure that we get to appreciate any change in the operating environment.

Schedule and summary of US Research Trip

| Topic of coverage | Companies visited | Impact on Australian Companies |

| Social gaming | Electronic Arts, Activision, Glu Mobile, Take2Interactive, Zynga, Eilers | Aristocrat |

| Wine industry | Bronco Wine Company, V2 Wine Company | Treasury Wine Estate |

| US building industry | James Hardie Investor Day | James Hardie |

| Oil & Gas | BHP, Conoco Phillips, Shell, Schlumberger, Anadarko, Fluor | BHP, Woodside, Oil Search |

| US Consumer related companies | Coke, P&G, Colgate, UPS, Kroger, PECO Pallets, Visy/Pratt industries | US economy, inflation, Brambles, Amcor, CCL |

The US economy is motoring along. Inflation risk to the upside given the very low unemployment rate and the fiscal stimulus

Following a research trip last year, we were aware corporates were seeing a marked increase in input costs, mainly labour and freight. At that stage in the cycle, driving this increase in cost were changes to minimum wages by certain states and a general lack of available labour. This year, whilst those headwinds still exist, corporates were seeing much more pressure from input costs – whether from tariff related increases in steel for instance or oil-based raw materials. The more labour-intensive sectors of the economy such as the construction industry continued to see pressure on availability of tradesmen (electricians apparently one of the hot spots).

The buoyant conditions have clearly fed into capital markets, with corporate finance businesses booming and SME confidence very high. The level of M&A activity is expected to be elevated and ongoing for at least another 12-18 months, with Trump’s tax cuts lifting valuations. Restructuring activity, conversely, is at historical low levels. There is plenty of leverage in the economy; but because of the strong economic conditions, there is not much financial stress at this point.

Rates are likely to keep going up and will remain a headwind for financial assets. Valuations will matter

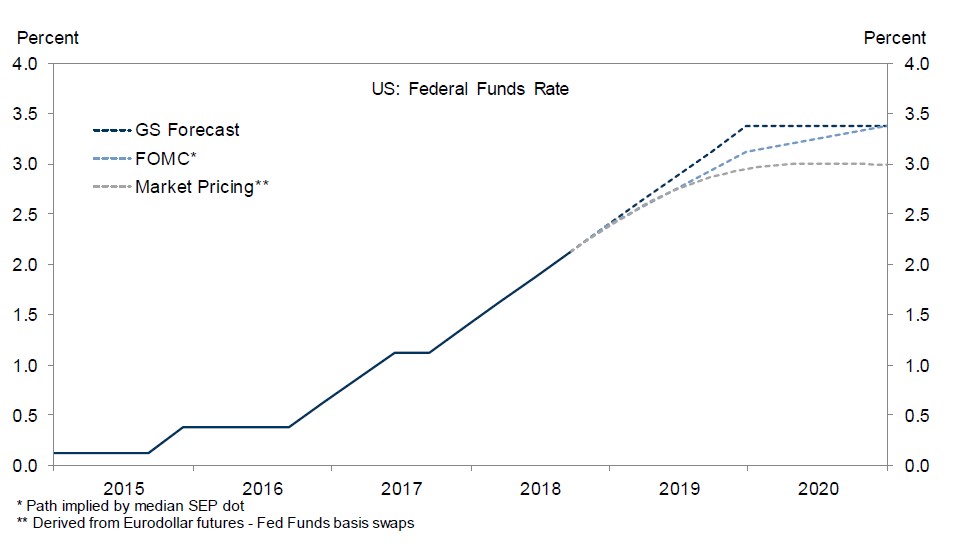

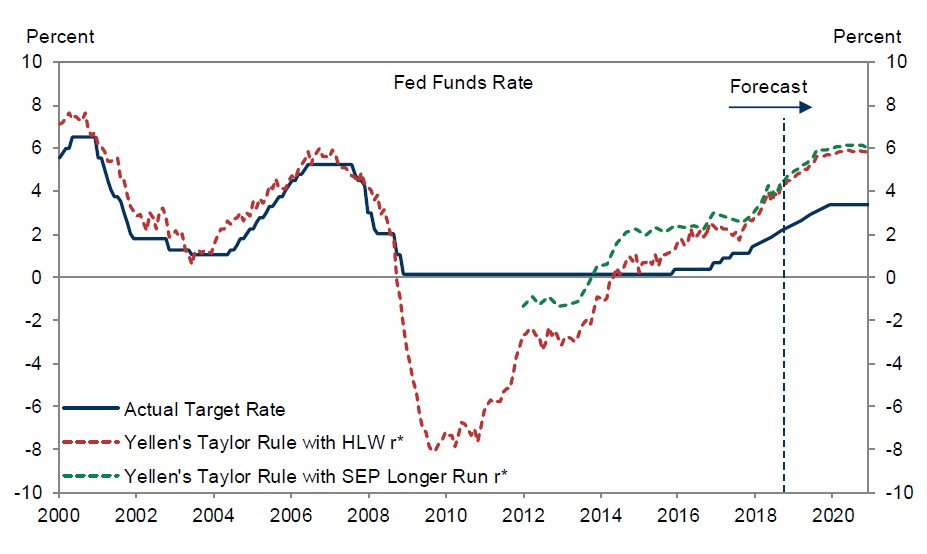

The US bond market is still under-pricing the Fed dot plots. As seen in the two charts below, Chart 1 shows the current view of interest rates. Chart 2 shows where the Fed thinks it should be based on the Yellen Taylor rule which indicates the Funds Rate should be 200 bps higher.

Chart 1: Forecast Fed Funds Rate

Source: Goldman Sachs

Chart 2: Forecast Fed Funds Rate (Yellen Taylor Rule)

Source: Goldman Sachs

Slots, social games and Aristocrat

On this trip, we met with/or spoke via conference calls with Electronic Arts, Activision, Glu Mobile, Take-Two Interactive, Zynga and also with industry experts Eilers. We also visited two of Aristocrat VGT’s largest tribal casino customers in Oklahoma.

A few key takeaways were:

- Our positive view on the social casino space was reinforced. Most of the corporates we spoke to felt that it was a very specialised field and one needed to understand real money gambling to succeed in that space. Growth has been strong, and this is expected to moderate to some degree.

- The evolution of the mobile casual gaming segment. It appears that there is a greater focus from the key industry players to improve the profitability of their social mobile businesses.

- Product development, monetisation methods as well as customer acquisition has become more data driven. All the companies spoke about increased usage of Artificial Intelligence and Business Intelligence tools to better understand customer profile

- All the corporates talked about the Fortnite phenomenon and quite upbeat on the flow on impact on their businesses – a larger pool of players have been drawn into the segment which they believe they can attract with their own content.

- Aristocrat has done a very good job integrating the VGT business since acquisition and has maintained an excellent relationship with the tribal casino operators. This is good news because both these properties, which are benefiting from their proximity to the fast-growing population corridor in Dallas-Fort Worth (less than 100 miles away), are planning significant expansion in the next 2-3 years. Given the strong VGT game performance, we expect Aristocrat to gain a good share of the expanded casino floors.

Houston Day with oil and gas companies

The key observation from these oil & gas meetings was a clear focus and discipline when it comes to capital allocation. Companies such as Conoco and Anadarko who were seen to be too conservative a few years ago are finally being rewarded for their capital discipline. The mood in these companies were significantly upbeat compared to prior visits when oil prices were falling sharply and they were being forced to shed people, sell assets and reduce debt.

All the companies were bullish on oil given the low capital spend and the high depletion rates. What has also surprised the oil companies is that despite the weakness in emerging markets particularly Latin America and places like Turkey, overall oil demand growth has remained robust. Forecasts are for demand to continue to grow between 1.4-1.8mm barrels in 2019. With the sanctions against Iran, the issues in Venezuela etc, oil supply will remain tight.

The BHP meeting was focused around the prospects of the oil division post the divestment of the US onshore assets. The divestments were on track and it is our expectation that the proceeds will be returned to the shareholders.

There was generally a more positive view towards the LNG market, with the demand outlook improving, mainly driven by ongoing consumption growth in China. Discussions were more positive on both greenfield and brownfield projects moving closer to FID. Shell talked about LNG Canada, as did Fluor who are in a JV with JGC to build that plant. Anadarko talked about their progress with their Mozambique LNG project. BHP were upbeat about their involvement in the Woodside-led Scarborough project in Western Australia.

James Hardie Investor Day, Orlando

James Hardie is one of only a handful of successful Australian businesses that created a market leading position (external siding) in the US market from scratch. All of this was achieved organically and it’s an impressive Australian success story in the US market. It was an important time to meet with the company as Louis Gries, the key architect of the James Hardie success story, had recently announced his retirement. His successor Jack Truong has been appointed, first as President and COO and will take over from him early next year. The business had a few false starts in succession, but this is the real deal. Louis is 65 years old and will retire this time.

The new CEO Jack Truong summed up his view of the values of James Hardie in four key points:

- James Hardie has the number 1 position in its chosen markets: In external fibre cement siding the company has built market leading positions in North America, Asia-pacific (Australia, New Zealand) and the Philippines. Whilst Fermacell, the recently acquired business, holds a number 1 position in fibre gypsum across its European markets.

- Manufacturing knowhow: James Hardie has the largest plants in those markets and has the biggest throughput. This helps its scale and profitability relative to its competitors.

- Maniacal focus on one thing: James Hardie are very good at being focused. The company has historically been able to point the entire organisation to achieve any goal set by the top management.

- Strong management team: Jack believes that he has inherited a very strong group of senior managers from Louis.

The key short-term risk to James Hardie is that the US market for new housing has stalled and this has resulted in the de-rating of the US home builders stocks over the last few months.

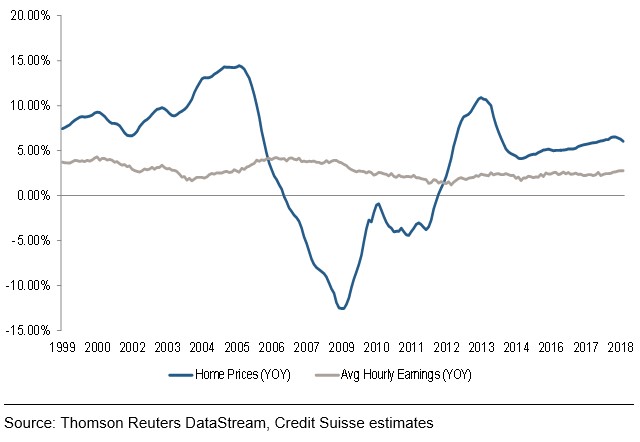

Chart 3: US home prices outpacing wage growth

Chart 4: US Mortgage rates rising

Interest rates have moved significantly, with the 30-year fixed mortgage rate at 4.75% – the highest since 2011. House prices have moved up, and this coupled with higher rates, is impacting affordability. Also, there is not enough land available at the right price for new community developments. In addition, most of the younger cohort are burdened with student debt and therefore can’t necessarily afford a mortgage.

In our view, US new housing starts will ultimately reflect household formation and despite the short-term headwinds mentioned above, there is a need for housing starts to increase further. In that regard, we continue to hold James Hardie as a core portfolio position given its strong industry position and proven track record of success.

Author: Raaz Bhuyan, Principal and Portfolio Manager